Our Cash Position ~ Important Read !

- VOICE of SCOV

- Jan 22, 2024

- 7 min read

Updated: Feb 10

REBUTTAL to

Our CASH POSITION

Update 2026:

Kurt, the writer of this report, ran for the board, but was viciously demeaned and ostracized by members of a group called 'CREW'. They mainly consist of previous board and committee members, those who had brought us into such financial constraints in the first place. They saw themselves fit to undermine anyone who dared to set the records straight.

Kurt didn't win. Unfortunately we have a community of residents who will believe any sort of propaganda from current or previous leadership because they don't pay attention to the business affairs of their HOA. They assume all is well. Gone, however are those days of blind trust. We have hope that within time, now with new management, there will be some improvement and more equitable board members WILL get elected. Kurt's reports exposed these previous leaders' money-wasting, over-spending and fiscal irresponsibility. Therefore, they were highly threatened by him and what he professed. Had Kurt won a position on the board, our community would have been on a good road for financial healing and responsibility. He said he wouldn't give up and would run again. He was able to secure a position on the Finance & Budget Committee, but later this year was offered such a good opportunity, he went back to working a full time job. He would have been a gem for our community. Maybe some day he will return to volunteer his expertise. As it stands now, as we approach a new year in 2026, nothing has much improved with our current leadership, as they sink their heels into the ground on spending multi-millions on pie-in-the sky plans for the money-pit called the Copper Bldg. All we can ask of you is until we have more reputable board people, you vote down anything they request of you.

________________________________________________

We are posting a rebuttal to the “Just the Facts” of Jan 18, 2024 and Tipster articles which states we have "plenty of cash".

This analysis was done by Kurt Egertson, a resident with 36 years in commercial and corporate banking. His most recent position was Chief Credit Officer of a $1.2 billion community bank. Kurt has intimate knowledge of Cash and Reserve balances. We should all be grateful for his analysis, as it is deep and thorough.

In contrast, look at the analysis from the others, who did not even provide a detailed cash flow analysis. They just say we have "plenty of money". Below is Kurt's open letter to the Board, submitted today on Jan 22, 2024.

Please make copies (pdf attached) and distribute them to your neighbors who may not be on social media, but whose finances will be impacted.

We need to be financially stable and secure as a Community.

Click the pdf below for a copy of the Open Letter:

Open Letter

To: Board of Directors

From: Kurt Egertson, Resident

MY REASON FOR WRITING

I spoke up at a recent meeting organized by people running for the open Board seats. I was immediately dismissed (directly and on-line) by numerous people as "not knowing the facts". So, I decided to do more in-depth analysis and complete my diligence. In the process I have heard plenty of bold statements being made to dissuade questions and assure all residents that they can ignore the questions, because everything is alright.

One simple example was the blurb “Just the Facts” in Thursday’s newsletter where it said we had a savings of $6.3 million and other cash of $1.7 million. Added up, that totals to $8.0 million. The clear implication is that we have lots of money! It is for each of us personally!

But,this $1.7 million number is misleading. Based on the November numbers it appears to include: (i) accounts receivable and (ii) inventory, which add up to about $400,000. If those accounts were cash, they would be labelled as cash. They are not cash. At November month end we had about $7.5 million in cash.

What is not clear: Is it a lot of cash for us? Is it enough cash for a community of our size?

MY CREDENTIALS

By way of my background: I have a Master’s in accounting and finance. I have spent 36 years in commercial and corporate banking, including some of the largest banking organizations in the country, spending the last 9 years as Chief Credit Officer of a $1.2 billion community bank. I have analyzed thousands of companies. The first and most important analysis is always cash flow.

MY FINDINGS IN SUMMARY

Our Asset Reserve Fund is really only $4.05 million and is underfunded compared to the 2021 third-party Asset Reserve Study. We stand at 51% of the recommended amount and our Policy is 60-70%.

Our non-Fund cash should get us through this year and into July (next year):

a. But just barely, and b. With no more spending from the Capital Fund or the Asset Reserve Fund this year.

The amount of cash we have is NOT enough for a community of our size: a. We will be hard pressed to restore our Asset Reserve and Capital Funds, and b. To attain a maintenance level of spending on existing assets, significant increases in revenue will be required.

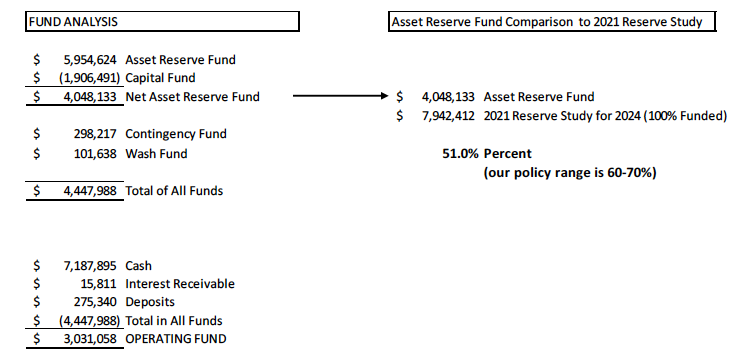

FUND BALANCES

We regularly publish that we have $5.9 million in our Asset Reserve Fund. We are not being honest with ourselves. Our approach ignores the negative $1.9 million balance in the Capital Fund. We know we ‘borrowed’ money from the Asset Reserve Fund for the Copper acquisition, which left the Capital Fund negative by $1.9 million. Analytically if we lent the $1.9 million to the Capital Fund from the Asset Reserve Fund, then let’s show it that way. The negative balance needs to be funded by the Asset Reserve Fund – at least to bring it to a zero balance. The simplest way to show it is: Net the two Funds.

The table below shows that the NET AMOUNT in the Asset Reserve Fund is really $4.05 million. As shown in the table, compared to the reserve study we are at 51% of our target. This is the clearest analysis. We robbed Peter to pay Paul. And we are really in violation of our own policy - recall that our Policy is to be funded 60-70%.

FUND ANALYSIS Asset Reserve Fund in Comparison to 2021 Reserve Study:

GIVEN OUR FUND BALANCES, WHAT CASH IS AVAILABLE FOR OPERATIONS

We need to keep our Asset Reserve Fund at $4.05 million and the other Funds at their current balances, which total $4.45 million. As the math shows in the table below, this leaves just over $3.0 million for our operating cash needs, what I call our Operating Fund. I am using November 2023 month end data.

CASH FORECAST ASSUMPTIONS

In researching my cash forecast, I met with four of the candidates who were then running for the board. I also reviewed the five-year plan that was included in the 2023-2024 Budget, as well as the 2021 Asset Reserve Study. One candidate also shared information he put together which, I believe, he developed based on discussions with the Controller.

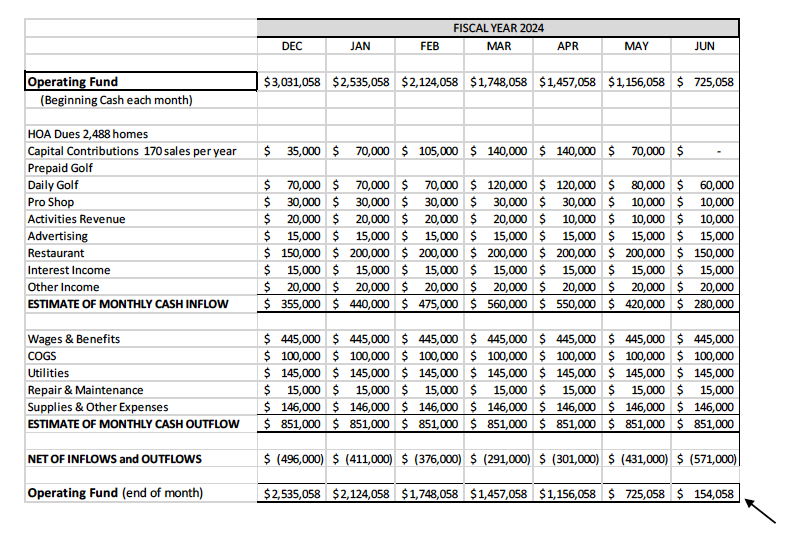

YEAR ENDING JUNE 2024

My numbers are all forecast and rounded. They are estimates.

I included no rate increases or inflationary cost increases this year, ending June 2024.

I built the model by month to account for the seasonality and to show some detail.

In some cases, I eyeballed the numbers and averaged the months.

I assumed no spending from any Funds (Asset Reserve or Capital) this year ending June.

The point of my cash forecast is to get a base-line, directional understanding of cash flows.

The following is a Summary using November month end data and running a cash forecast through the end of this year: June 2024. It shows that directionally, we have just enough cash to get through to July. But not by a wide margin. And, the forecast assumes no additional contributions to or spending from our Cash Fund Balances (savings). The model starts with the $3.0 million in the Operating Fund at December 1, 2023 and ends with $154,058 shown in the bottom right of the table. That is pretty tight.

As mentioned, there is room to refine these numbers. But I think the numbers are directionally quite accurate. Further, as mentioned, I have assumed no spending from our Asset Reserve Fund or any other Funds, including the Capital Fund. This suggests we are very tight on cash.

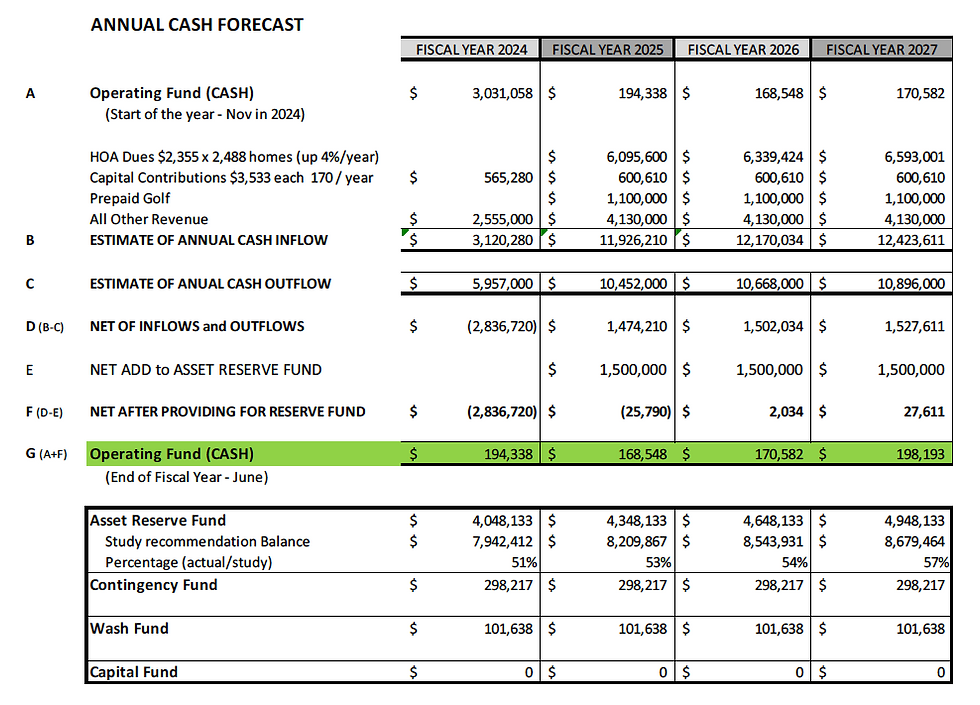

THREE YEAR FORECAST

In the next table, I show a summary of a much more detailed monthly cash forecast. I assumed:

Increases to HOA Fees of 4% per year. About $100 per residence.

The major sources of revenue are shown, with the rest lumped into “All Other.”

Cash outflows are lumped into one line item. Wages and Benefits increase about 4% per year.

In row labeled “E” (on left side), a $1.5 million contribution to the Asset Reserve is made each of three years. Maintenance spending from that Fund is assumed at $1.1 to $1.2 million per year, which can be seen in the changes to the Asset Reserve Balance in the bottom section.

The Operating Fund ends up with less than $200,000 in any period (green highlighted row).

The Asset Reserve fund does not achieve 60% Funding compared to Study data.

As mentioned, there is room to refine these numbers. But I think the numbers are directionally quite accurate. Further, as mentioned, I have assumed no spending from our Asset Reserve Fund or any other Funds, including the Capital Fund. This suggests we are

very tight on cash.

RECOMMENDATION

The Board should direct management to make necessary and difficult decisions to course correct:

The Board should direct management to provide, on a regular basis, a 12-month rolling cash forecast in simplified format on one page.

The Board should direct management to get an updated Asset Reserve Study completed as soon as possible.

Comments